Dumper trucks are tough machines, but they’re not immune to risk. From theft to tip-overs, the types of claims insurers see from UK construction and groundwork firms often follow a...

Plant & Machinery Insurance

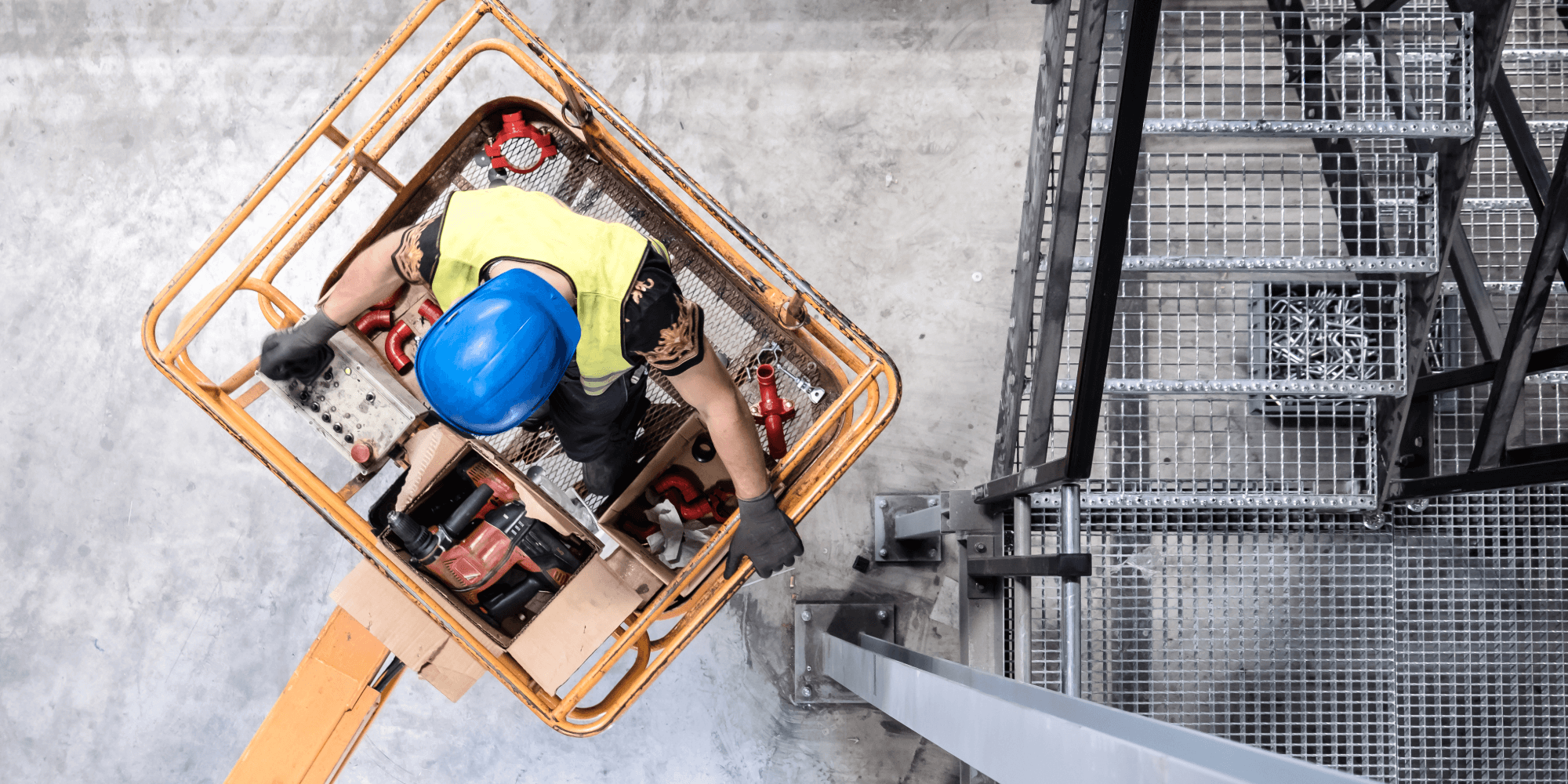

Whether you're a construction contractor managing heavy equipment or a tradesman hiring machinery for projects, Plant & Machinery Insurance (often referred to as contractors’ plant insurance) is vital to protect your valuable assets. This specialised cover safeguards your plant, from excavators, diggers and cranes to forklifts and cherry pickers against everyday risks like theft, accidental damage, fire, and vandalism.

As one of the UK’s leading specialists in Plant & Machinery Insurance, we leverage our strong relationships with top insurers to find you flexible cover at competitive prices. Our experienced team understands the construction industry and ensures you get the right protection for your machinery, so your business stays covered when it matters most.

START YOUR QUOTE

CALL US

As one of the UK’s leading specialists in Plant & Machinery Insurance, we leverage our strong relationships with top insurers to find you flexible cover at competitive prices. Our experienced team understands the construction industry and ensures you get the right protection for your machinery, so your business stays covered when it matters most.

OR CALL 0330 808 1905

How It Works

1

Request a Quote Contact our team or complete an online quote form. We’ll gather a few key details about your business, the plant machinery you use, and the cover you need.

2

Discuss Your Needs We’ll review your details, discuss your needs, and match you with the right cover based on your equipment.

3

Compare and Choose We compare quotes from leading UK insurers, explain your tailored options, and set up cover immediately once you choose the right policy.

Insurance Revolution's Reviews

Plant & Machinery Insurance: What You Need to Know

Plant & Machinery Insurance brings together essential protections to safeguard the machinery and equipment your business relies on. Standard commercial vehicle or property insurance often won’t cover specialised plant used on construction sites or other work environments. A dedicated plant insurance policy fills that gap by covering a wide range of risks specific to heavy equipment.

What does it cover?

In general, a Plant & Machinery Insurance policy will cover the cost of repair or replacement if your insured items are accidentally damaged, lost or stolen. This applies whether the equipment is on your site, in storage, or in transit between locations. For example, if an expensive excavator or forklift is damaged on site or a generator or cement mixer is stolen from a lockup overnight, your policy can compensate you so you can repair or replace it promptly. Plant insurance can also extend to cover attached tools and accessories, and many policies offer optional add-ons like continued hire cost cover (to pay for rental charges if hired plant is out of action) or road risk cover for mobile plant that travels on public highways.

Common Risks in Plant Operations

Construction and engineering firms face daily risks when using heavy machinery. Plant & Machinery Insurance helps protect against common threats like theft, damage and liability.

Theft and Vandalism: Plant equipment is a frequent target, especially overnight. Insurance covers stolen or vandalised diggers, loaders or other machinery, helping reduce downtime and financial loss.

Accidental Damage: Even skilled operators can cause damage. A toppled excavator or dropped tool can sideline equipment. With the right cover, repair or replacement costs are handled quickly.

Fire, Flood and Weather: On-site plant is vulnerable to fire, flood and storm damage. A strong plant insurance policy protects against these natural risks, ensuring your machinery is not left unusable.

Transit and Off-Site Risks: Machinery in transit or stored off-site can be damaged or stolen. Plant insurance includes transit cover, so your equipment is protected wherever it goes.

Third-Party Liability: If your machinery causes injury or property damage, such as a crane tipping over, the right policy can include liability cover to protect against legal claims and costs.

Without proper insurance, these events could cause serious delays or major costs. Plant & Machinery Insurance helps you recover fast, minimising disruption and keeping your business running smoothly.

Why Choose Insurance Revolution

Specialist Industry Expertise: We understand construction and engineering insurance. Whether it’s a single mini-excavator or a full fleet, our experienced brokers tailor cover to suit your plant and machinery needs.

Access to Top UK Insurers: As an independent broker, we compare quotes from leading UK providers to find competitive prices and robust cover, saving you time and avoiding unnecessary extras.

Flexible, Tailored Cover: Need protection for owned or hired-in plant, multiple sites or seasonal work? We customise policy limits, add-ons and payment options so you only pay for what you need.

Dedicated UK Support: Our friendly UK-based team is here for policy advice, updates or claims help, delivering fast, personal service when you need it most.

Claims Assistance & Risk Management: We liaise with insurers to ensure swift payouts and minimal disruption. We also offer security and safety advice to help reduce claims and manage costs long term.

OR CALL 0330 808 1905

Third-Party Liability Cover

This covers injury or property damage claims against you if one of your business vehicles causes an accident. It’s the core of any motor policy and meets your minimum legal obligations for driving on UK roads.

Comprehensive Cover

Full comprehensive insurance covers damage to your own vehicles as well, not just third-party claims. If your plant machinery is damaged in an accident (even if it’s your driver’s fault) or by fire, theft, or vandalism, your policy can pay for repairs or replacement so your business isn’t left footing the bill.

Any Driver & Multiple Driver Policies

With an “any driver” option, any qualified employee can drive your insured vehicle (useful if you have rotating staff or a pool of machines). Alternatively, you can name specific drivers for a lower premium. We’ll help you choose the best option for your situation, ensuring anyone who needs to drive is properly covered.

Breakdown & Roadside Assistance

Optional breakdown cover can be included to get your vehicles back on site if they break down. From roadside repairs to towing and recovery, this add-on saves you time and money (and stress) if a work vehicle unexpectedly fails while out on a job.

Courtesy Vehicle (Hire Vehicle) Cover

If one of your business vehicles is in for repair after an accident, courtesy vehicle cover provides a temporary replacement. This means you can continue your operations with minimal interruption, for example, keeping deliveries on schedule or maintaining client visits while your car/van is being repaired.

Windscreen & Glass Cover

Covers the repair or replacement of cracked or shattered windscreens and windows. Commercial vehicles often rack up high mileage and experience heavy usage, so chips and cracks are common. With this cover, those inevitable windshield damages can be fixed quickly at no extra cost, ensuring clear vision (and legal compliance) at all times.

Tools, Equipment & Goods Cover

If you carry work tools, stock, or cargo in your vehicle, we can arrange cover for those items (often via a Goods in Transit or tools cover add-on). This protects the value inside your van, truck or plant machinery, for instance, if your equipment is stolen from the vehicle or goods are damaged in a collision, you can recover the costs. Don’t let a theft or spill wipe out your expensive gear or inventory.

Legal Expenses Insurance

Legal cover can be included to help with costs if you face any legal disputes or claims after a vehicle incident. This might fund your legal defence or help recover uninsured losses. Essentially, it provides access to expert legal support and covers fees so one accident doesn’t turn into a mountain of legal bills for your business.

Business owners who rely on vehicles need to manage many moving parts, literally. Your drivers are out on public roads, your schedule (and income) depends on vehicles running smoothly, and accidents can happen to anyone.

That means the right cover isn’t just helpful, it’s essential. We’ll shape your policy around how your business operates, whether you have a single plant vehicle, a pool of shared vehicles, or an entire fleet of machinery. With Insurance Revolution, you get a partner who understands the risks you face and ensures you’re protected every mile of the journey.

FAQs

Anyone using high-value machinery or equipment for business purposes should consider Plant & Machinery Insurance. If you’re a building contractor, civil engineer, landscaper, farmer, or any tradesperson operating plant (from small diggers and forklifts to large cranes and bulldozers), this cover is essential. Standard commercial insurance policies won’t typically cover specialised plant at work sites. Even if you only use hired equipment occasionally, you are usually liable for it while it’s in your possession, so without insurance you’d have to pay out of pocket for any theft or damage. In short, if losing or damaging a piece of machinery would hurt your business financially, then you need plant insurance to stay protected.

A typical plant insurance policy covers your contractors’ plant and equipment against “All Risks” of physical loss, theft or accidental damage, anywhere in the UK. This usually includes risks like fire, flood, storm damage, collapse, overturning, theft, vandalism and other sudden unforeseen events.

For owned plant, it pays for repair or replacement if your machinery is damaged or stolen (at the site, in transit, or even while stored). For hired-in plant, it covers the hire charges or replacement costs you’d owe the rental company if something happens to their equipment on your watch. Some policies automatically include cover for equipment attachments and accessories, as well as debris removal costs if a machine is wrecked on-site.

It’s important to note that if any insured machines will be driven on public roads, you should have a Road Risks extension for third-party motor liability(since by law road-going vehicles require that). Plant insurance can often be customised with add-ons too, for example, adding breakdown cover, increased limits, or hiring out cover if you rent your own plant to others. We’ll help you choose the right mix of coverages so that everything important is protected and no gaps are left in your policy.

Yes – even if you hire plant infrequently, you should still have insurance for it. When you rent equipment from a hire company, the contract will almost always state that you are responsible for loss or damage during the hire period. The hire company’s insurance won’t cover you; in fact, they will expect you to reimburse them for any stolen or damaged kit. Hired-In Plant Insurance is designed for this exact situation. It can be arranged for short-term hires (even on a per-project basis) or as an annual policy covering all equipment you hire in over the year.

The insurance will cover the cost of repairing or replacing the hired machine if something goes wrong, as well as any continuing hire charges (since the hire firm might charge you rent until a damaged item is fixed or a stolen item is replaced). Without this cover, even a one-off incident, like a rented mini-digger being vandalised or a hired generator catching fire could leave you facing thousands of pounds in bills. It’s simply not worth the risk. We can set up affordable hired-in plant cover to keep you protected, no matter how occasionally you rent machinery.

The cost of plant insurance depends on several factors, so it can vary widely. Insurers will look at the value of your equipment, the types of machinery and what they’re used for, as well as where they are kept or operated (security and location can influence risk). They’ll also consider whether the plant is owned or hired, if you ever hire your own equipment out to others, how often it’s in use, and your past claims history. As a rough idea, premiums for an annual contractors’ plant policy might start around a few hundred pounds for a small business, but larger companies with multiple machines could pay more.

The good news is there are ways to keep premiums cost effective. Keeping your kit secure (e.g. using immobilisers, trackers and secure lock-ups) can earn you discounts. Maintaining a good claims record and implementing safety measures (like regular maintenance and operator training) will also make insurers more inclined to offer better rates.

We’ll help you find the most competitive quote by shopping our panel of insurers and making sure you’re only paying for the coverage you need, nothing more. Remember, the price of insurance will always be far cheaper than the cost of replacing a stolen excavator or facing an uninsured liability claim, so it’s a smart investment in your business’s continuity.

Absolutely. Plant & Machinery Insurance isn’t a one-size-fits-all product, and that’s exactly why working with a specialist broker is beneficial. We take the time to understand your operations so we can customise the policy around your specific requirements. You can choose the coverage limits and options that make sense for you. For example, you might opt for: cover on a replacement as new basis for newer equipment, add hired-in plant cover up to a certain value, include transit cover if you frequently move machines between sites, or add public liability cover into the package.

If you have multiple pieces of plant, we can either list them individually or set a blanket limit for unspecified equipment (useful if your inventory changes often). Policies can also be arranged for short-term projects or on an annual basis covering all projects – whichever suits your business model.

Our role is to ensure you’re fully protected without paying for extras you don’t need. We’ll guide you through the available options (like increasing cover during peak periods or adding seasonal hire cover) and craft a tailored insurance solution that gives you peace of mind that every angle is covered. In the end, you get a bespoke policy that aligns perfectly with how you operate, so you’re not over-insured or under-insured, but just right.

OR CALL 0330 808 1905

Helpful Articles & Updates

Explore expert insights on Plant & Machinery Insurance. From equipment protection to operational safety and theft prevention, our latest guides help UK contractors and access platform operators stay informed, compliant, and covered on every job.

Owned vs Hired Dumper Truck Insurance – What’s the Difference?

Whether you own your dumper trucks or hire them in for specific jobs, the type of insurance you need can differ significantly. Confusing these two could leave you underinsured, or...

Do I Need Dumper Truck Insurance? A Quick Guide for UK Site Operators

Dumper trucks are essential for moving heavy loads on construction and groundwork sites but they’re also high-risk machines prone to accidents, theft and damage. Whether you own or hire a...

Electric vs Diesel Forklifts – Does It Affect Insurance?

As UK businesses shift toward greener operations, electric forklifts are becoming more popular but does the type of forklift you use affect your insurance policy or premium?

In this blog,...

Forklift Liability Insurance: What It Is and Why It Matters

A forklift accident can cause serious injury, property damage and costly downtime and if you're found liable, the financial consequences can be severe. That’s why forklift liability insurance is one...

Do I Need Forklift Truck Insurance? A Guide for UK Businesses

Whether you run a warehouse, construction site, or manufacturing facility, forklift trucks are essential for moving heavy loads. But are they legally required to be insured? And what kind of...

How to Prevent Excavator Theft and Lower Your Insurance Premium

Excavators and mini diggers are among the most stolen types of plant equipment in the UK. With units valued anywhere from £15,000 to over £200,000, one theft can devastate your...

Mini Digger vs Large Excavator Insurance – What’s the Difference?

Not all diggers are treated equally when it comes to insurance. Whether you’re operating a compact mini digger for landscaping or a large excavator for major groundwork, the type of...

Do I Need Digger Insurance? A Quick Guide for UK Operators

If you operate a digger or excavator whether it’s a mini digger, tracked machine or wheeled unit, having the right insurance isn’t just a box-tick exercise. With high theft rates,...

Top Crane Insurance Risks (and How to Avoid Them on Site)

Crane operations are some of the most high-risk activities on a construction site. A single incident can lead to serious injury, project delays, and six-figure insurance claims. Whether you're operating...

Is Hired-In Crane Insurance Enough? What Operators Should Know

Hiring a crane for a lifting job might seem straightforward but when something goes wrong, who’s responsible? If you're hiring cranes under CPA or similar terms, assuming the crane hire...

Mobile Crane vs Tower Crane Insurance: What’s the Difference?

Crane operations come with high risk and high value, so getting the right insurance matters. But not all cranes are covered the same way. If you operate mobile cranes or...

How to Stay Compliant When Using Cherry Pickers on Site or Road

Using cherry pickers or mobile elevated work platforms (MEWPs), comes with strict safety and legal responsibilities. Whether you're operating on a private site or driving on public roads, non-compliance can...

What Does Cherry Picker Insurance Cover? Everything You Need to Know

Whether you own a single MEWP or manage a fleet of access platforms, Cherry Picker Insurance is essential to protect your business from the high risks associated with working at...

5 Common Plant Equipment Insurance Claims and How to Avoid Them

Whether you operate a single excavator or manage a fleet of machines across multiple sites, Plant & Machinery Insurance is vital for protecting your business. But do you know what...

How to Insure Hired-in vs Owned Plant – What’s the Difference?

If your construction business uses heavy machinery, understanding the difference between hired-in plant insurance and owned plant cover is essential. Many UK contractors assume their policy protects everything, but if...

Do I Need Plant & Machinery Insurance? A Simple Guide for UK Contractors

Whether you're operating a mini excavator on a private site or managing a fleet of heavy construction vehicles across the UK, understanding your insurance obligations is essential. This guide breaks...